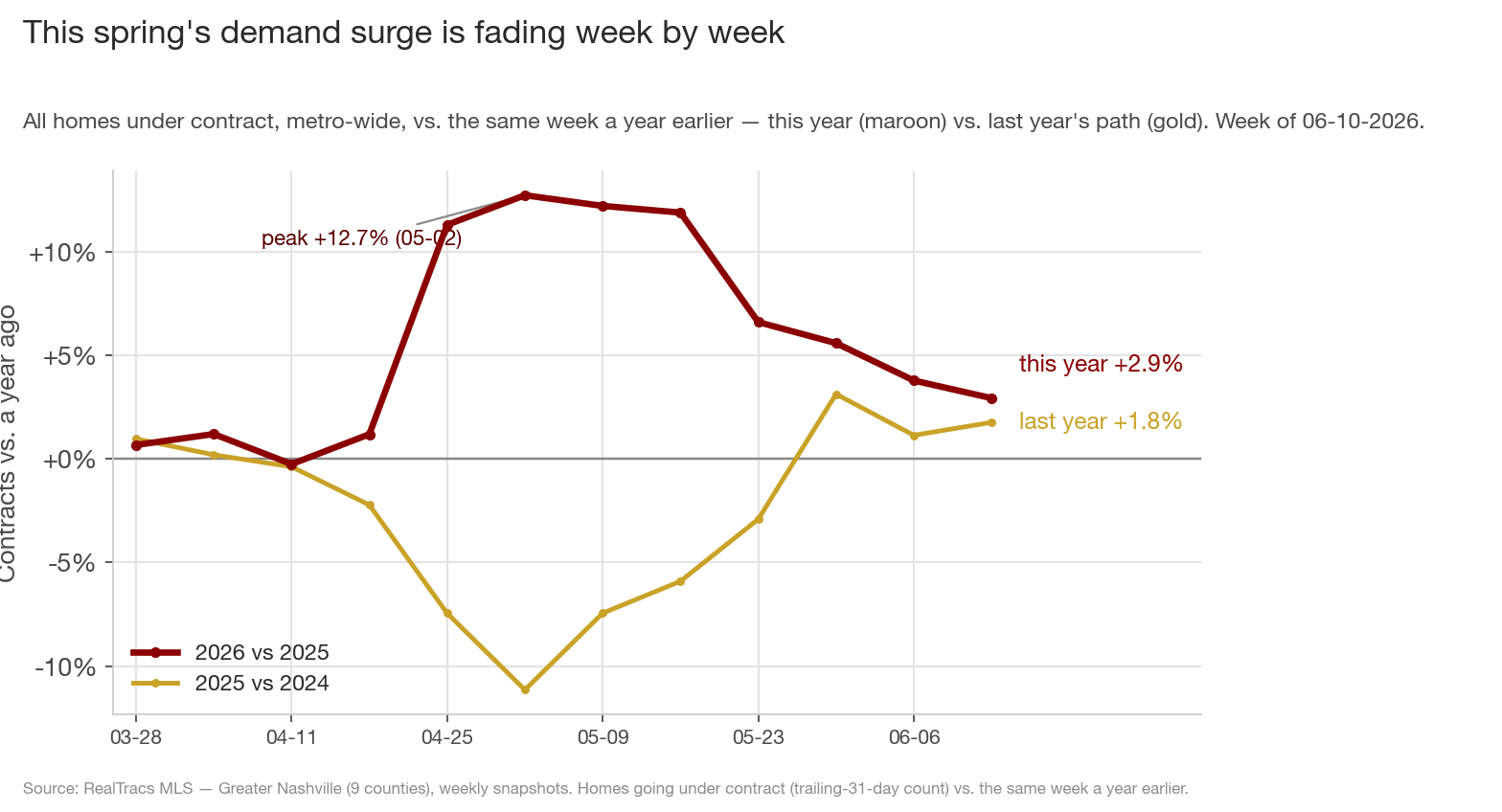

Five weeks ago, Greater Nashville demand was running its hottest stretch of the year: homes going under contract metro-wide were up +12.7% over the same week a year earlier. That growth has fallen every single week since — six straight lower readings: +12.2%, +11.9%, +6.6%, +5.6%, +3.8%, and now +2.9%. In count terms, the metro was signing 366 more contracts than a year ago at the May 2 peak; this week it's +88. At the average pace of the last five weeks, that cushion is gone before the end of June.

This isn't a one-segment story, and that's the point. On Monday I wrote about the move-up price band rolling over; this is the wider view, and it's worse than a band story. The fade shows up in the metro topline, in raw counts, and across geography: Davidson and Sumner — two of the four biggest counties — have flipped negative, and all four majors are decelerating at once. Here's the picture, and the honest caveats that go with it.

1. The fade — against last year's climb

The maroon line is this year: metro-wide homes going under contract versus the same week of 2025. It peaked at +12.7% on May 2 and has bled down to +2.9% — 3,094 contracts against 3,006 a year ago, a margin of just 88 homes across nine counties.

The gold line is the killer detail, because it answers the obvious objection: isn't demand supposed to fade after the spring peak? In raw counts, yes — but this is a year-over-year comparison, which nets the calendar out. And over these exact same weeks last year, the year-over-year line was moving the opposite direction: 2025 improved from −11.1% in early May to +1.8% by June 10. This year is fading through the very stretch where last year was recovering. The two lines have nearly converged — this year's "surge" is now barely a percentage point better than last year's grind.

One honest caveat baked into that same gold line: part of why 2026 looked so strong in late April is that the comparison was easy — April 2025 was the soft patch. As the base stiffened into June, some air was always going to come out of the growth rate. But that's an argument about the size of the peak, not the direction since — which brings us to the raw counts.

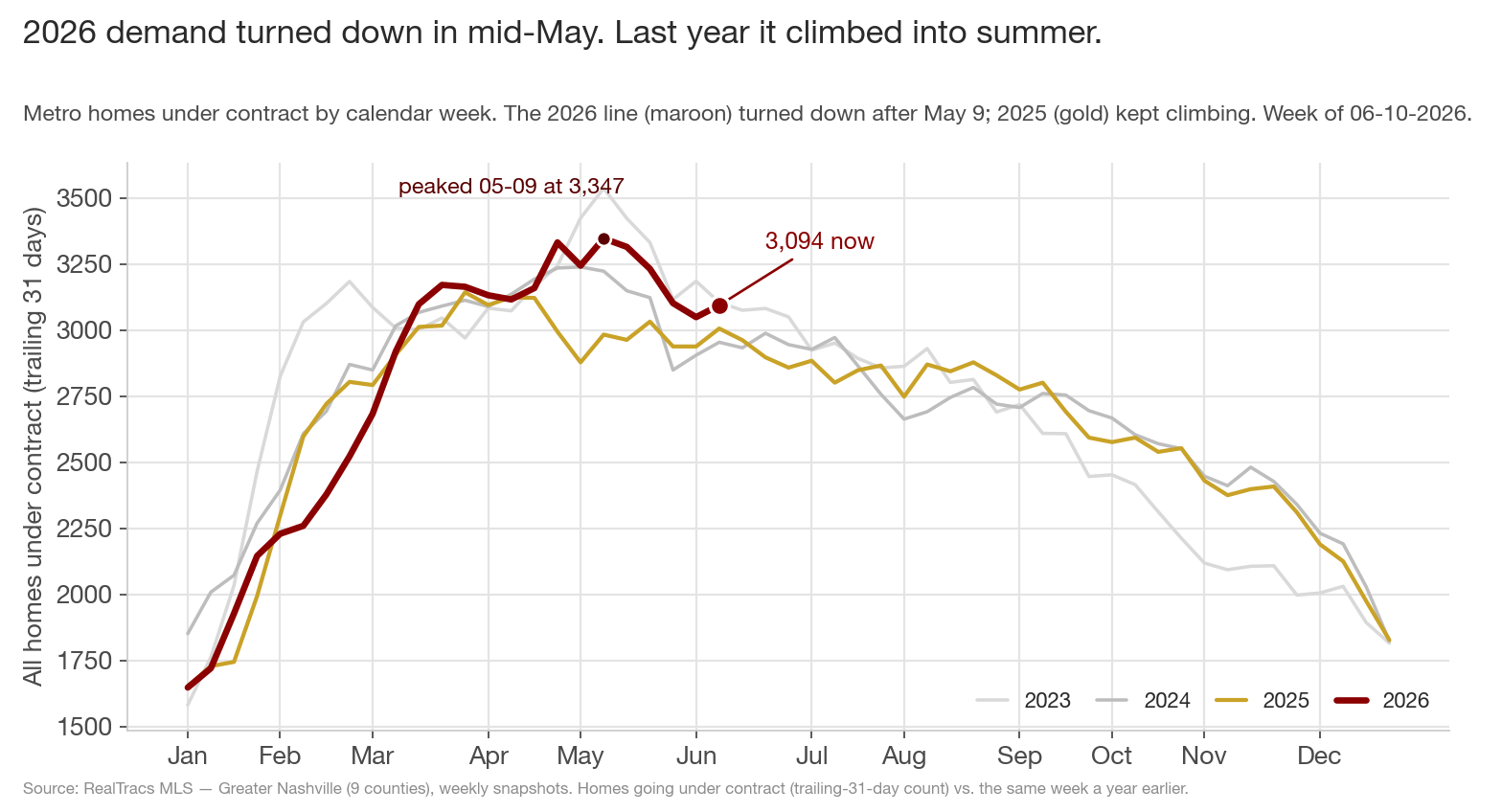

2. It's not the calendar — demand turned down in levels, too

Strip out the year-over-year math and just count contracts. The 2026 line (maroon) peaked at 3,347 on May 9 and has dropped to 3,094 — down 253 contracts, −7.6%, in a month. Over the same calendar stretch last year, the 2025 line (gold) went from 2,983 to 3,006 — still climbing into mid-June. The 2024 and 2023 lines drift sideways-to-lower through this window, so some late-spring sag isn't unusual — but pairing a falling count with a rising prior-year base is exactly how a +12.7% growth print turns into +2.9% in five weeks.

Worth saying plainly: 3,094 is still the second-busiest June 10 reading in the four years of data (2023 was 3,105), so this is a decelerating market, not a collapsed one. The story is the turn, not the level.

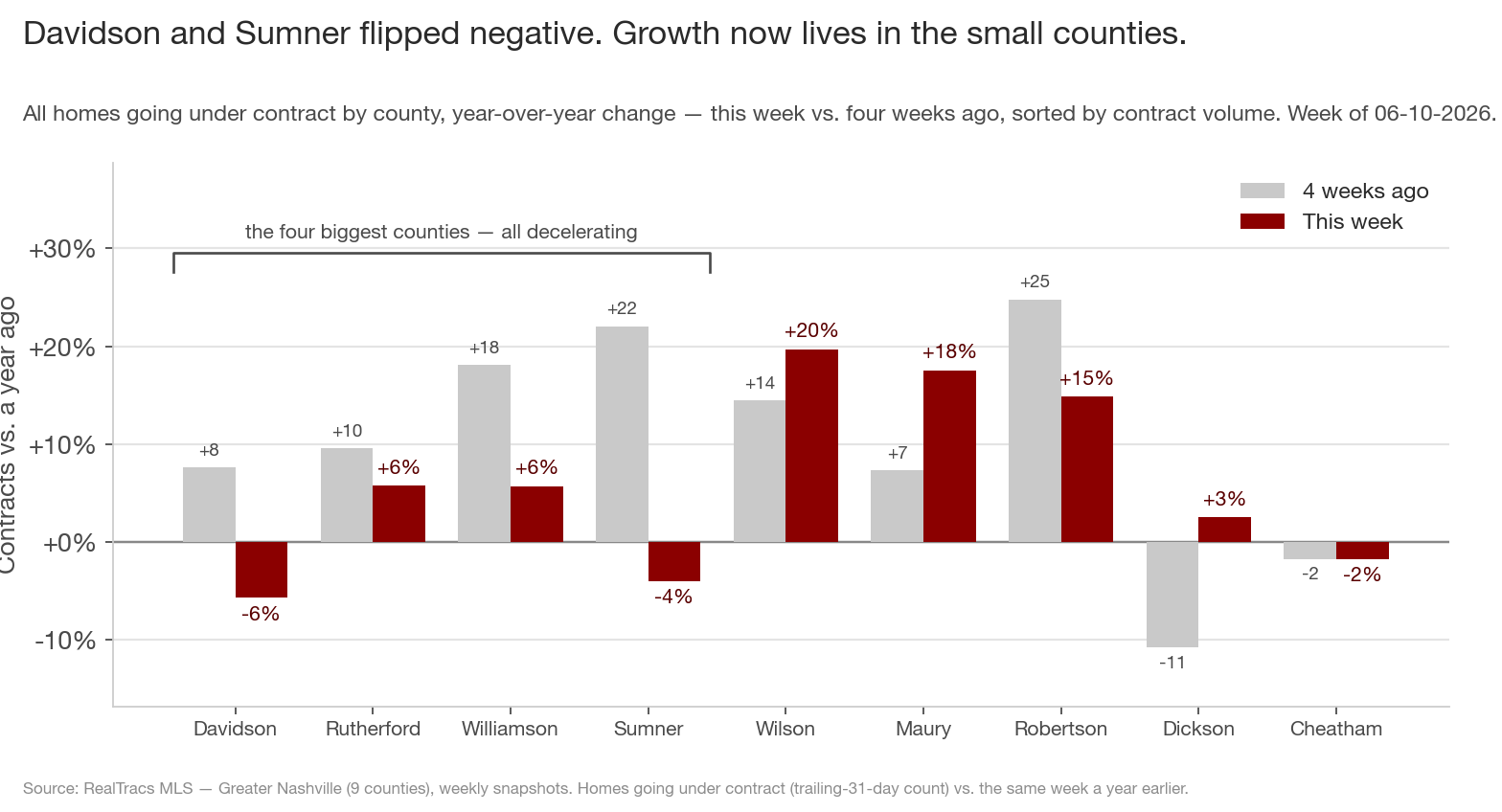

3. The four biggest counties all rolled over at once

Four weeks ago, every one of the four biggest counties was growing: Davidson +7.6%, Williamson +18.1%, Rutherford +9.6%, Sumner +22.1%. This week: Davidson −5.7%, Williamson +5.7%, Rutherford +5.8%, Sumner −4.0%. All four decelerated; two flipped outright negative. Those four counties carry 73% of the metro's contracts — when they all turn at once, the topline goes where they go.

What growth remains has retreated to the smaller, cheaper, outer counties: Wilson +19.7%, Maury +17.6%, Robertson +14.8%. That's a familiar shape — it rhymes with the price-band barbell from Monday's post, where the budget tiers held up while the $500K-and-up bands cooled. Buyers haven't vanished; they've moved down-market and out-of-county, where the median price is lower and the new-construction incentives live.

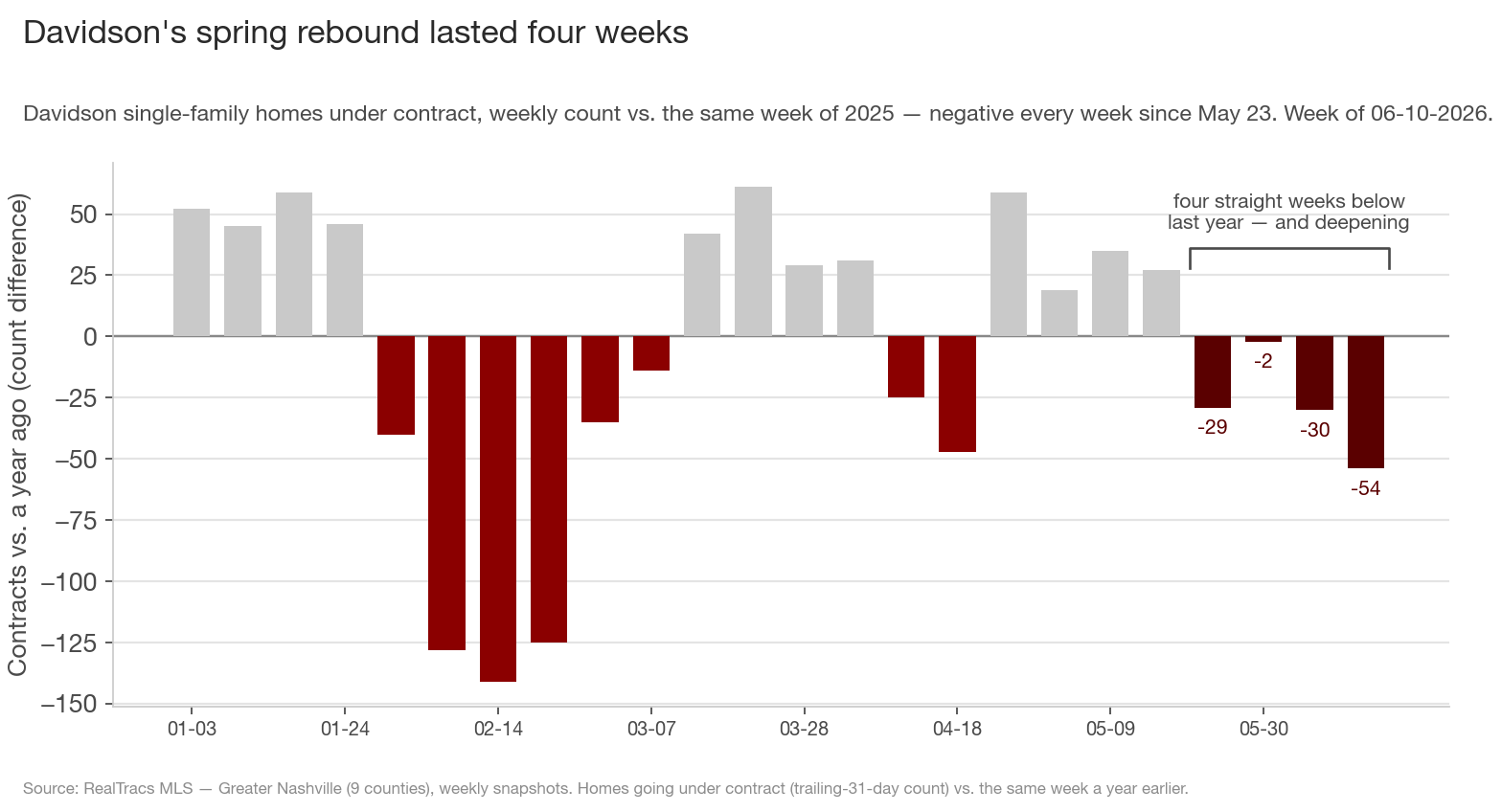

4. Davidson: the rebound that lasted four weeks

Davidson County — the metro's biggest market, and the county that just set a record $550K single-family median — has now signed fewer single-family contracts than a year earlier for four straight weeks: −29, −2, −30, and now −54 (706 vs. 760, −7.1%). Each week of the streak has been deeper than the week before except the near-tie at May 30, and −54 is Davidson's deepest weekly deficit since late February, back when the whole market was still digging out of the winter slump. The all-property number tells the same story: −56, also the worst since February.

Two things make this more than chop. First, the spring rebound it ended was short — Davidson ran above 2025 for exactly four weeks, April 25 to May 16, and has now spent four weeks below it. Second, the level is low outright: 706 single-family contracts is the fewest for an early-June week in all four years of the data (2023: 739, 2024: 755, 2025: 760). Record prices, shrinking forward demand — that pairing is exactly what the price-versus-volume divergence I flagged in the median-record post looks like when it shows up in the demand data.

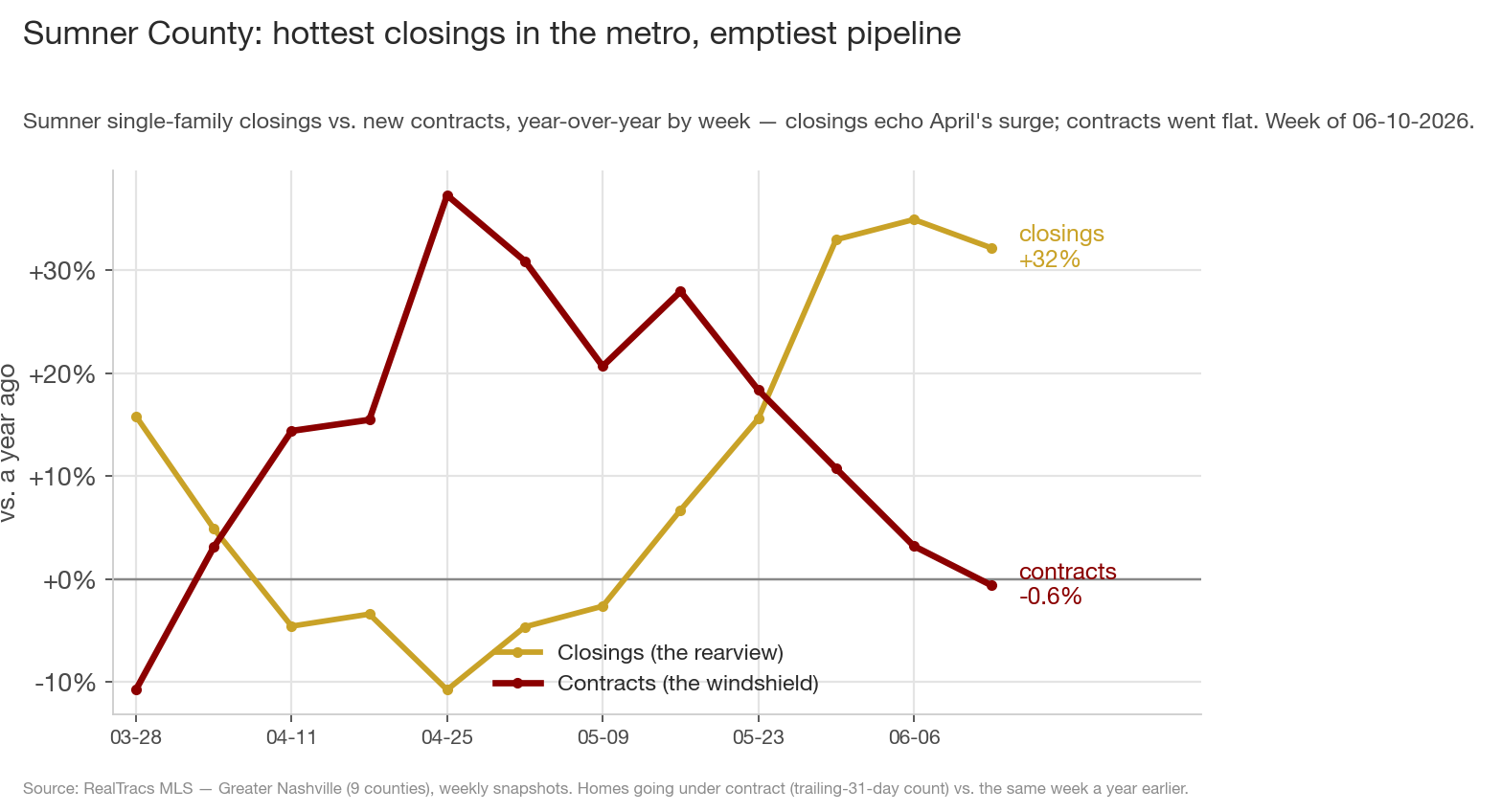

5. Sumner: the rearview and the windshield

If you only looked at closings, Sumner County would be the hottest market in Middle Tennessee: 337 single-family closings against 255 a year ago, +32.2% — the strongest of all nine counties. But closings are the rearview mirror. Those 337 homes mostly went under contract in April, when Sumner's contract growth peaked at +37.3%. The windshield view is the maroon line: contract growth has since collapsed — +27.9% four weeks ago, −0.6% now. The scissors crossed in late May.

Honesty note: Sumner's contracts were also slightly negative at this same week last year, so the minus sign itself isn't unprecedented — it's the 38-point swing since late April that's the signal, the sharpest reversal of any county. The prediction this chart makes is mechanical: contracts lead closings by six to eight weeks, so Sumner's +32% closing boom should fade toward zero by late July. If it doesn't, something unusual is happening in Sumner — either way, we'll know within two months.

What this adds up to

- The metro demand surge is fading fast — contract growth fell from +12.7% to +2.9% in six straight weekly declines, while raw counts dropped 253 from the May 9 peak.

- It's not seasonal. Over these same calendar weeks last year, year-over-year growth was improving, and last year's raw counts were still rising in mid-June.

- It's broad. All four of the biggest counties — 73% of metro contracts — decelerated at once; Davidson (−5.7%) and Sumner (−4.0%) flipped negative. Growth now lives in Wilson, Maury, and Robertson.

- Davidson is leading the market down: four straight negative weeks, its deepest deficit since February, and the fewest early-June single-family contracts in the four years of data — in the same county that just set a record median price.

- The price dimension matches the geography. Every single-family band from $500K up decelerated over the past month — $500K–$750K from +12.7% to +2.2%, $750K–$1M from +36.9% to −12.6%, $1M–$2M from +23.1% to +11.4%. Even $2M+ came off the boil, from +71% to a still-enormous +60%. Only the two bands under $500K held or improved.

For sellers, the uncomfortable part is the lag: closings still look great — Sumner's are up 32% — but closings are April's market. The buyer pool that determines your outcome is the June one, and it's thinning by the week, fastest in Davidson, Sumner, and the $750K–$1M band. Price to the windshield, not the rearview. For buyers, leverage is shifting your way for the first time since winter, and quickest in exactly the places that were frenzied in April. For agents and builders, the dashboard metric for the next two months is pendings, not closings — closings will keep flattering the market into July no matter what demand does.

Here's the falsifiable part. The metro's year-over-year contract margin is +88 and has been shrinking by 50–60 a week for five weeks. If that pace holds, Greater Nashville prints its first negative demand week since February (April 11's −8 blip aside) before the July 4th weekend. If instead the line stabilizes in the +1% to +3% range and the big counties claw back to flat, then this was a plateau after an easy-comp spring, not a rollover — and I'll write that follow-up. Watch the metro contract line for the next three weeks; it's the single number that settles it.

Data through the week ending June 10, 2026, Greater Nashville (9 counties: Davidson, Williamson, Rutherford, Wilson, Sumner, Maury, Dickson, Cheatham, Robertson). "Contracts" are a trailing-31-day count of homes going under contract, compared with the same week of the prior year; metro and county figures cover all property types unless noted as single-family. Closings are a trailing-31-day count of closed sales. Source: RealTracs MLS.