Greater Nashville builders closed 696 newly built homes in the trailing month, the fewest for late June in the four years of data, down 17% from 2023 and 16% from 2024. Over the exact same stretch, resale closings climbed to 2,638, now 10% above their 2023 level and up 14% over last year. Split every closing into one of two buckets, newly built or resale, and only one bucket is still shrinking.

The tempting read is "demand is cracking." It isn't, and I should know. Earlier this month I wrote that new-construction closings had caught up (+9.4% year-over-year). That number was real but the framing was soft: it was measured against a tariff-depressed 2025, and against 2024 builders' closings were never caught up at all. The honest story is narrower and more interesting. Builders held onto their buyers and their prices; what they gave up was volume, letting their closing count slide to a cycle low. And the pullback is not spread evenly across the metro. Here it is, chart by chart.

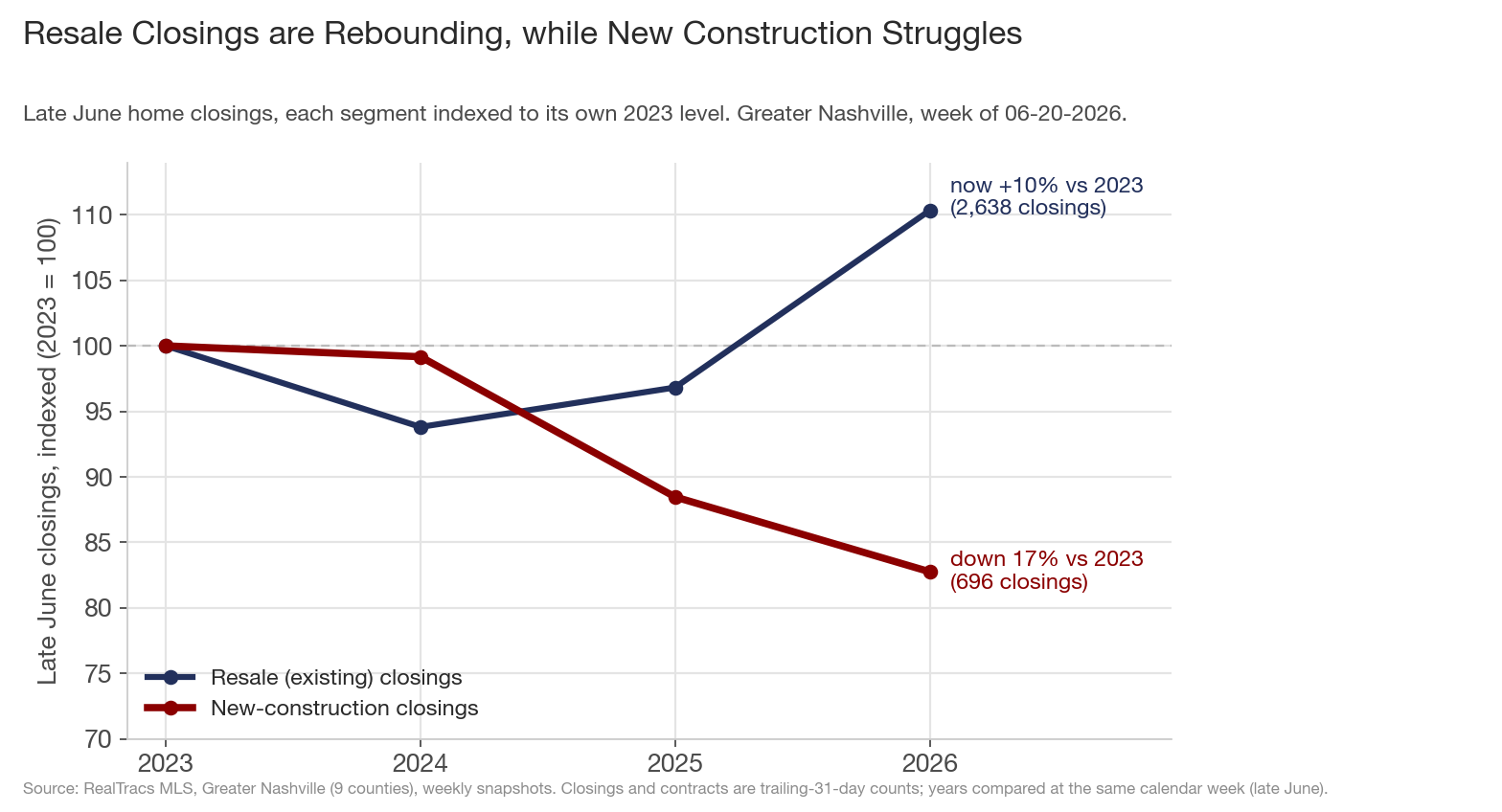

1. Resale Closings are Rebounding, while New Construction Struggles

Index each segment to its own 2023 late-June level and the divergence is clean. Resale dipped to 94 in 2024, then recovered all the way back and through, to 110 now: 2,638 closings, a full 10% above where it sat two Junes ago. New construction went the other way: 100 to 99 to 88 to 83. Builders are closing roughly a sixth fewer homes than they were two Junes ago, and the line is still pointed down.

That's why the metro aggregate looks merely soft rather than healthy: resale is carrying it, and new construction is the drag. New construction's share of all closings has slipped from 26% in 2023 (27% in 2024) to 20.9% now, from about one in four homes sold to one in five.

This is also the cleanest answer to the "is it just the tariff base?" question that has distorted every spring-2026 comparison. Closings reflect contracts written one to three months earlier, so the 2025 base here is the post-Liberation-Day trough, an easy comp. New-construction closings are down 6.5% even against that depressed base, and down about 17% against a normal 2024 and 2023. The weakness survives every baseline; it isn't an echo.

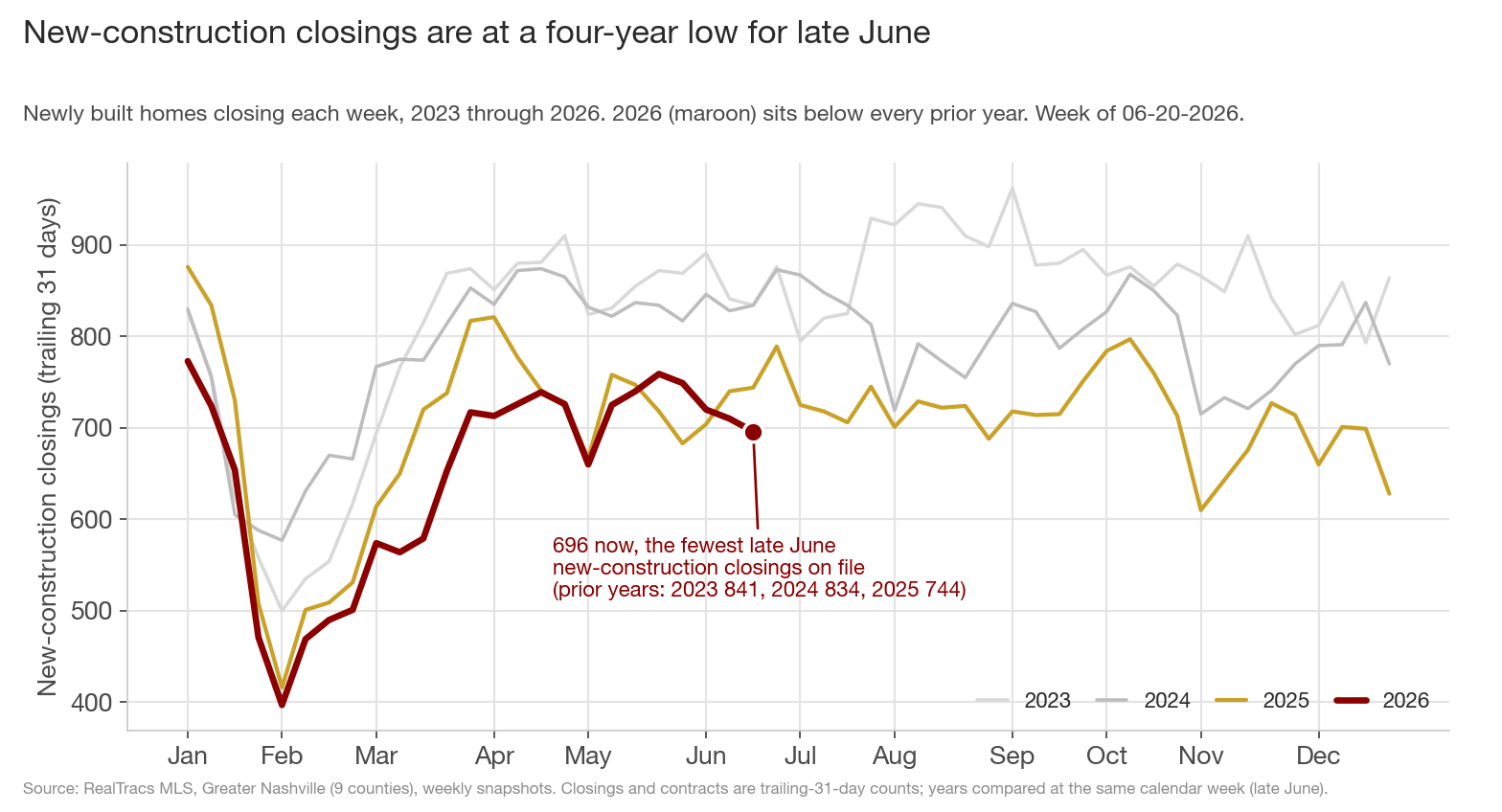

2. The fewest new-construction closings for late June on record

Stacking the four years week by week makes the same point seasonally. Every prior June, new-construction closings ran in the mid-700s to mid-800s; 2026 (the maroon line) has peeled away below all of them and sits at 696, beneath 2025 (744), 2024 (834), and 2023 (841). It is the lowest late-June reading in the data, and unlike a one-week blip, it has been grinding lower for a month: 759 in late May, then 749, 720, 710, and 696 now.

A note on what this measures: closings are a rear-view mirror. A home closing in late June went under contract back in roughly April. So this chart is really a picture of where builder deliveries have landed after the 2023-24 building boom worked through, and they've landed low.

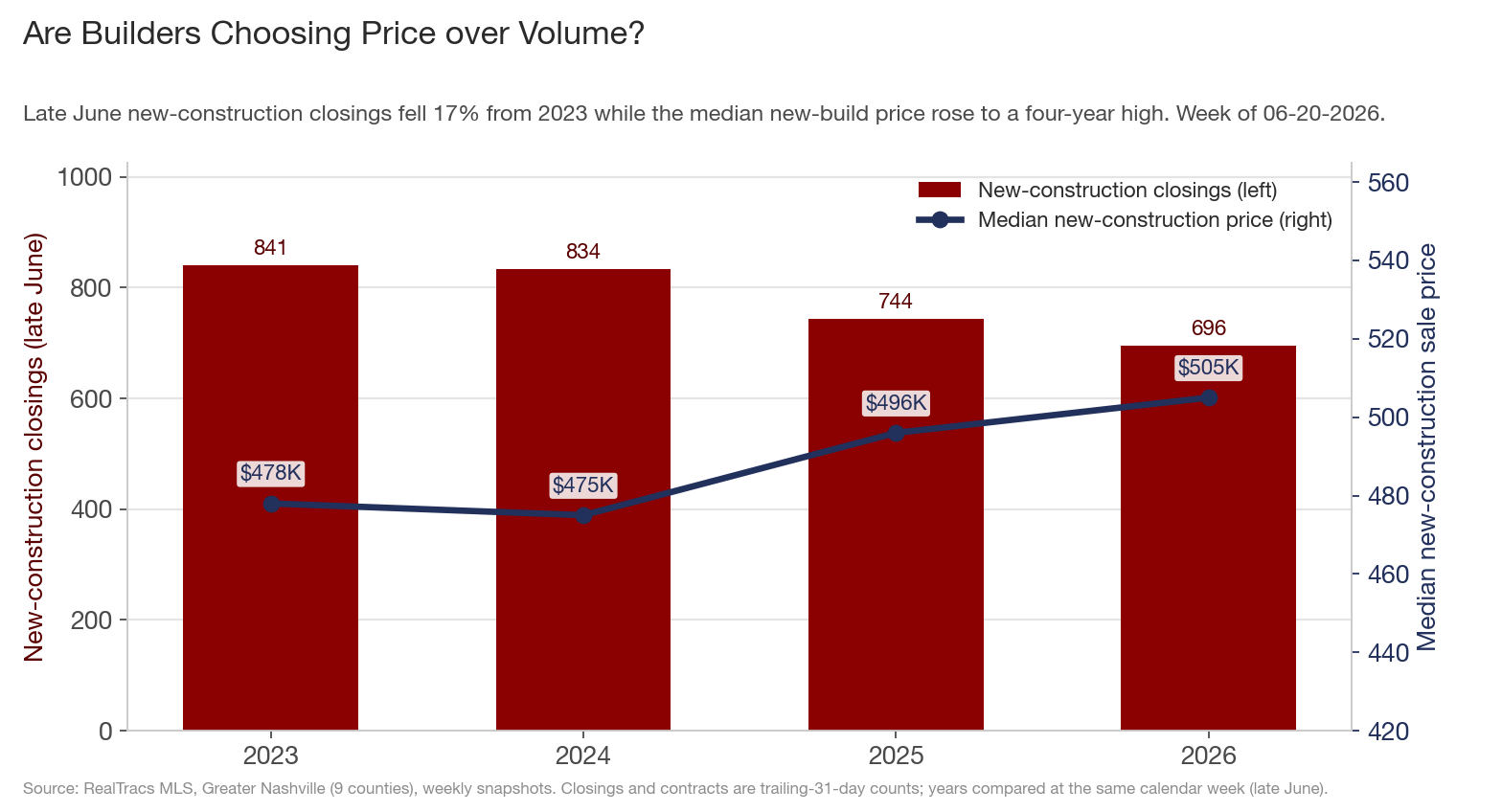

3. Are Builders Choosing Price over Volume?

Here's the part that separates this from a distress story. As closings fell 17%, the median new-construction sale price rose to $505,000, a four-year high, up from $478K in 2023 and $475K in 2024. Builders sold fewer homes at higher prices on purpose, rather than discounting their way to volume.

The price-cut data confirms it. Only 21% of new-construction listings carry a price cut right now, near the low end of its four-year range. On the resale side, 43% of listings have cut. That contrast is the whole story in one number: resale sellers met the market on price and moved the volume; builders held their price and moved less of it. It shows up in price per square foot too: new-construction PPSF is holding (+0.4% year-over-year) while resale's is slipping (-1.2%). In a market where carrying costs and incentives eat margin fast, a lot of builders are choosing to defend the number.

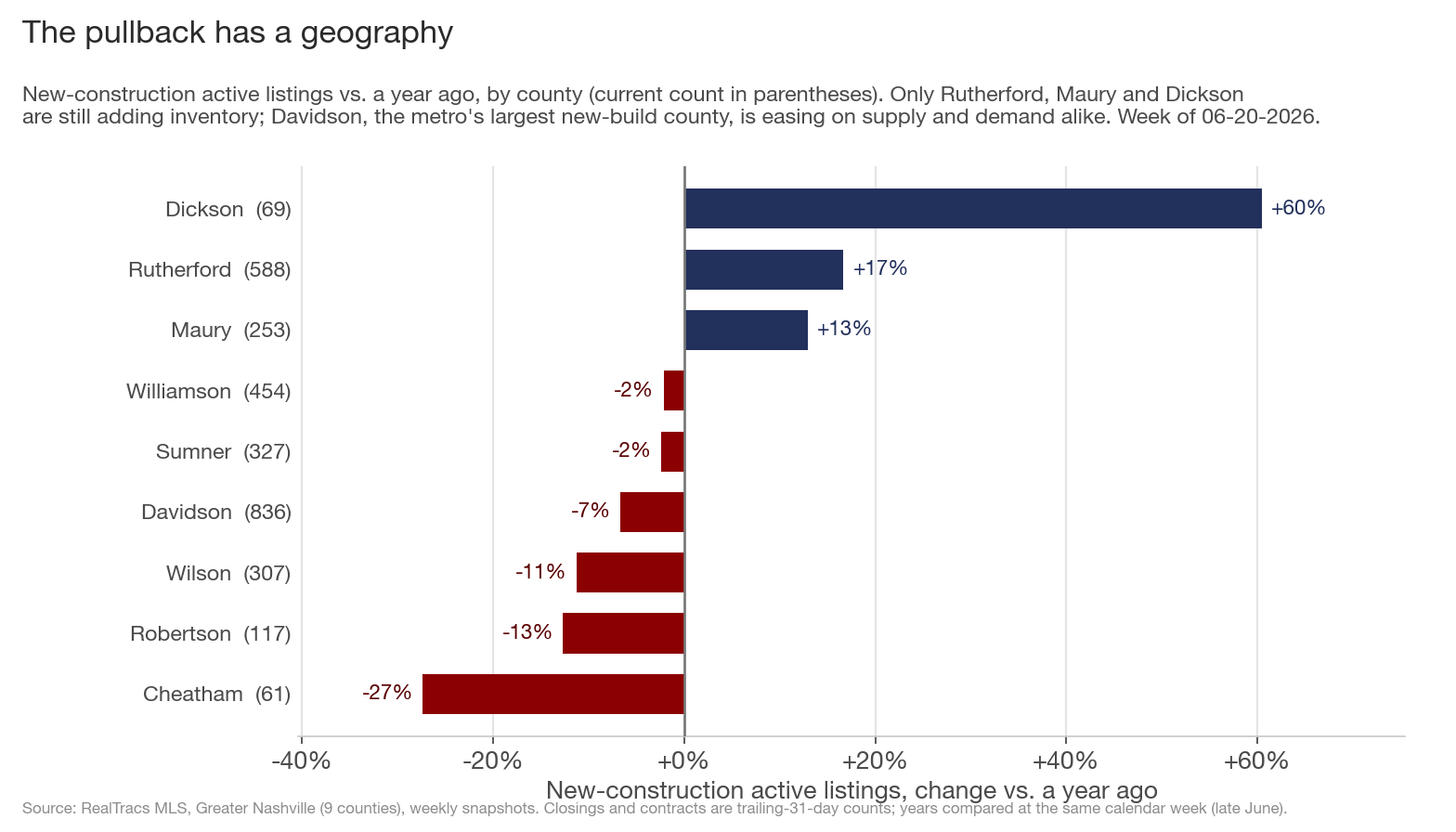

4. The pullback has a geography

The slowdown isn't uniform, and where it is and isn't tells you something. New-construction active inventory is rising in just three of nine counties: Rutherford +17%, Maury +13%, and Dickson (+60%, though off a tiny 69-listing base). Everywhere else it's flat to falling.

The clearest pullback is in the metro's biggest new-build county. Davidson, with 836 active new-construction listings (more than any other county), is easing on both sides of the ledger: inventory down 7%, and demand cooling with it (new-construction closings -20% year-over-year, contracts -13%). Wilson is down 11%. Even Williamson, the priciest new-build market in the region at a $1.37M median, has flattened (-2%).

The exception is the tell that this isn't a collapse: Rutherford (Murfreesboro) is booming on both sides, inventory +17% and closings +23%. The affordable I-24 growth corridor is still absorbing everything builders put up, while the urban core cools. Read together, the metro's new-construction drag is concentrated in Davidson and the rural fringe; builders are still leaning into the cheaper, faster-growing exurbs to the southeast.

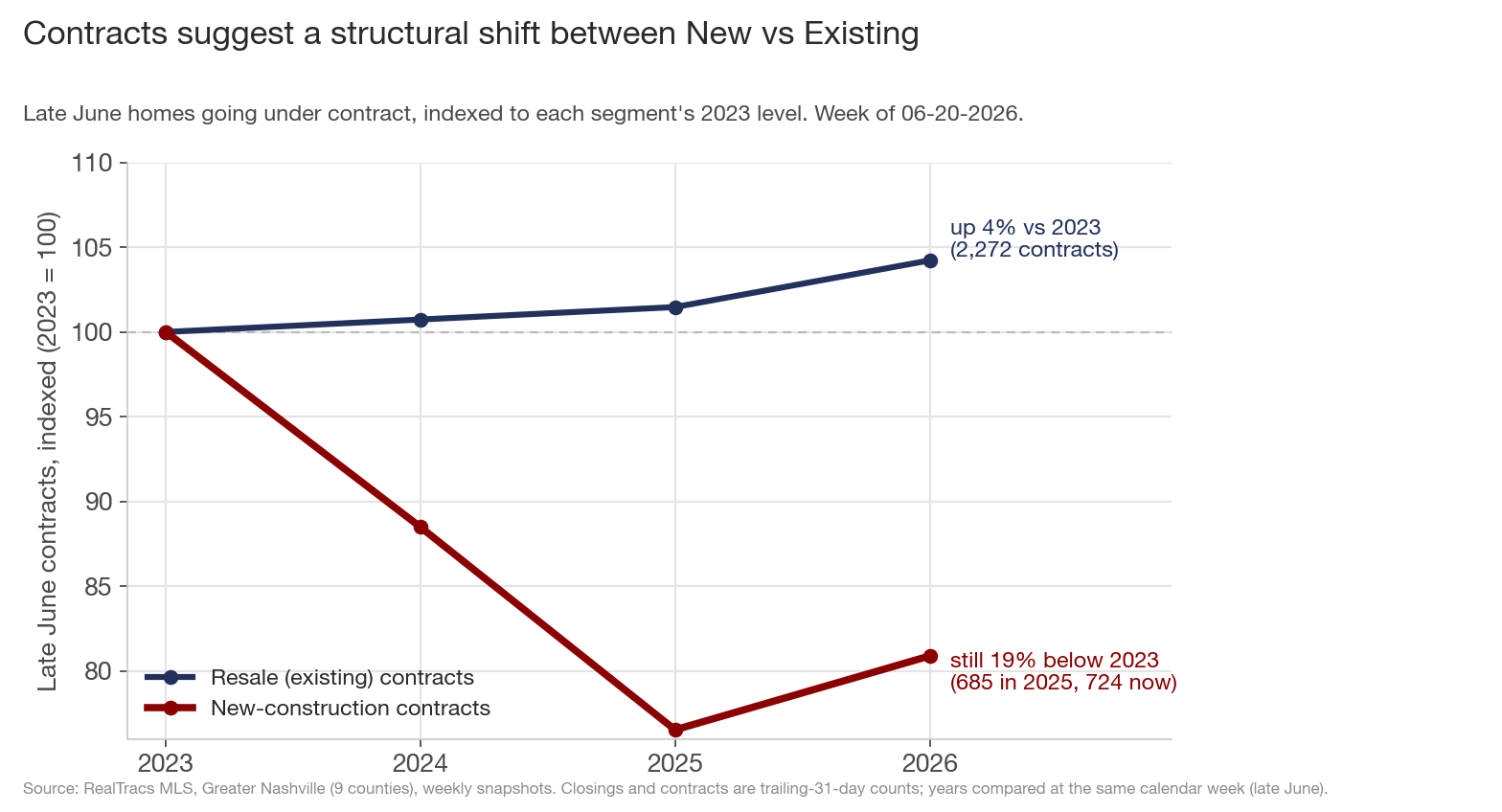

5. Contracts suggest a structural shift between New vs Existing

If you want to know whether June's low closings rebound in August, look at contracts, which are forward-looking, versus closings that went under contract as far back as 60 to 90 days ago. They point to a new, lower plateau. New-construction contracts fell from a 2023 baseline of 895 to a low of 685 in 2025, and sit at 724 now, still about 19% below 2023, with no recovery back toward it. Resale contracts did the opposite, climbing to 104% of their 2023 level (2,272 this June, up 3% over last year).

So new-construction demand didn't collapse; it reset to a lower level around 2024-25 and has held there. With the pipeline still a fifth below 2023, the low closing count is the new running rate rather than a seasonal wobble that snaps back next month. Builders calibrated to it: new active listings are flat year-over-year (-0.6%), the one inventory line in the metro that isn't climbing, while existing listings are up 11% and condos up 19%.

Why might this be happening? The sections above describe what changed. The harder question is why builders specifically pulled back while resale climbed. The data here cannot prove cause, and the real answer is probably a mix, but three forces stand out, and each one points back toward the same buyer.

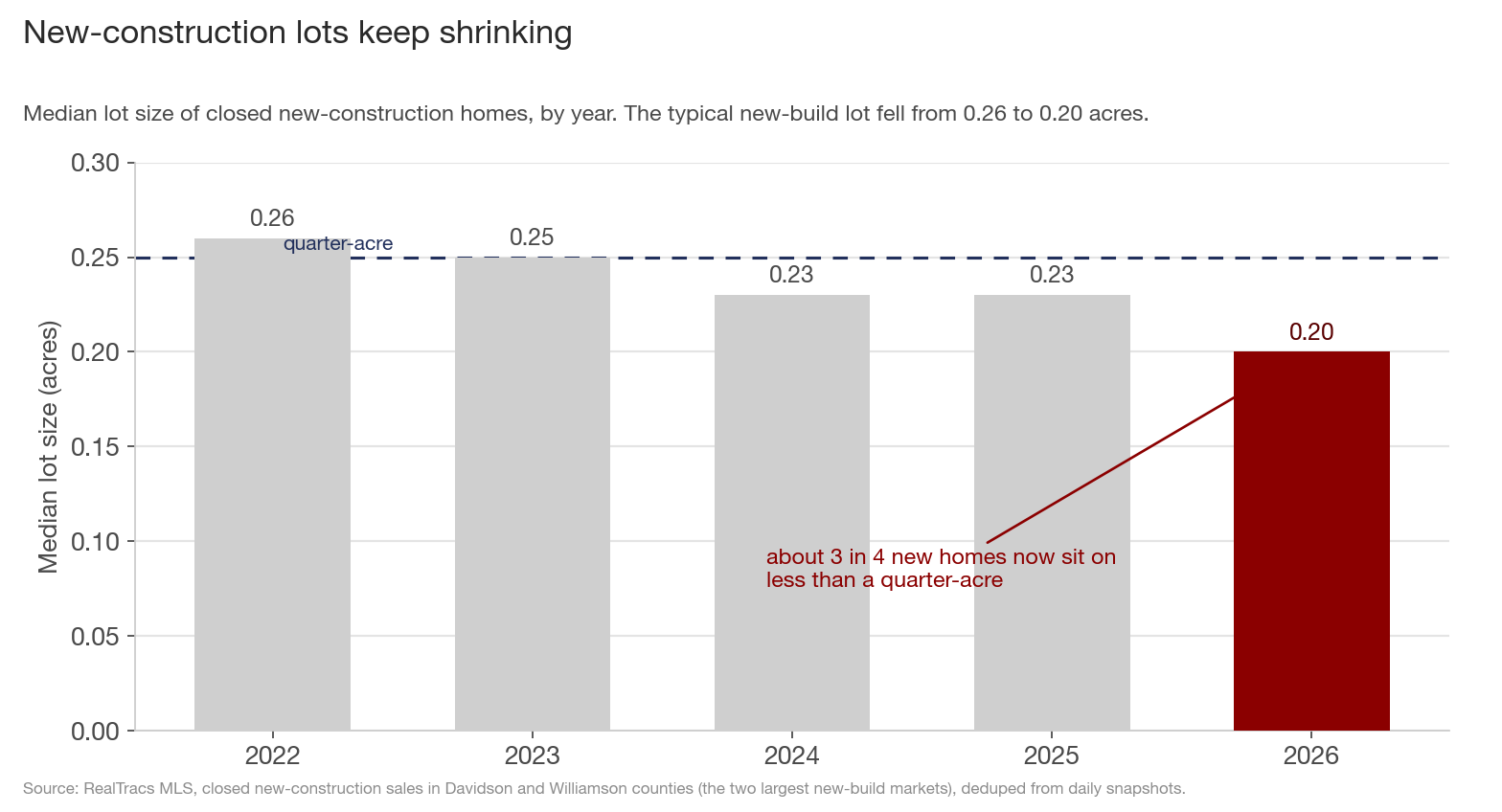

6. Are buyers paying more for less land?

One quiet shift is what a new home actually gives you. The median lot under a closed new-construction home in Davidson and Williamson counties has shrunk every year, from 0.26 acres in 2022 to 0.20 now, and roughly three in four new homes sit on less than a quarter-acre, against about 55% of resale homes. As land and development costs climbed, builders did the rational thing and put more homes on each acre, leaning into townhomes, infill, and tight subdivisions.

That keeps a new home within reach on price, and it also narrows the reason to choose new over resale. A move-up buyer who wants a yard, a garage, or room between neighbors increasingly finds it on the resale side, where the typical lot is larger and the inventory is now growing 11%. As the new-construction product converges toward smaller and denser, the premium buyers will pay for "new" gets thinner. (Lot figures here are Davidson and Williamson, the two largest new-build counties.)

7. Is the new-build reputation taking on water?

A second force is harder to measure but well documented: the reputation of the national volume builders who put up most of Nashville's new homes. Complaints and defect litigation against the three largest production builders, D.R. Horton, Lennar, and PulteGroup, all active across Middle Tennessee, have been climbing. D.R. Horton's reserves for construction-defect claims rose 57% to $1.1 billion between fiscal 2022 and 2025, as the Wall Street Journal reported, and investigations including Hunterbrook's "House from Hell" and Moneywise's reporting have catalogued homeowners alleging cut corners, cheaper materials, and poorly supervised subcontractors as builders pushed volume. Closer to home, contractor and home-improvement disputes top the complaint list at Tennessee's Division of Consumer Affairs, which the state Attorney General flagged in 2025.

The builders push back, and the pushback is fair to print: they argue defects show up in a small fraction of the homes they deliver and usually trace to subcontractors or aggressive litigation rather than a systemic drop in quality.

I cannot measure how much any of this moves a Nashville buyer's decision, and none of it is proof about a specific local home. But when the dominant new-construction product carries a national brand with a rising defect-claim bill, and buyers suddenly have a growing pile of resale homes to choose from instead, reputation is a plausible thumb on the scale.

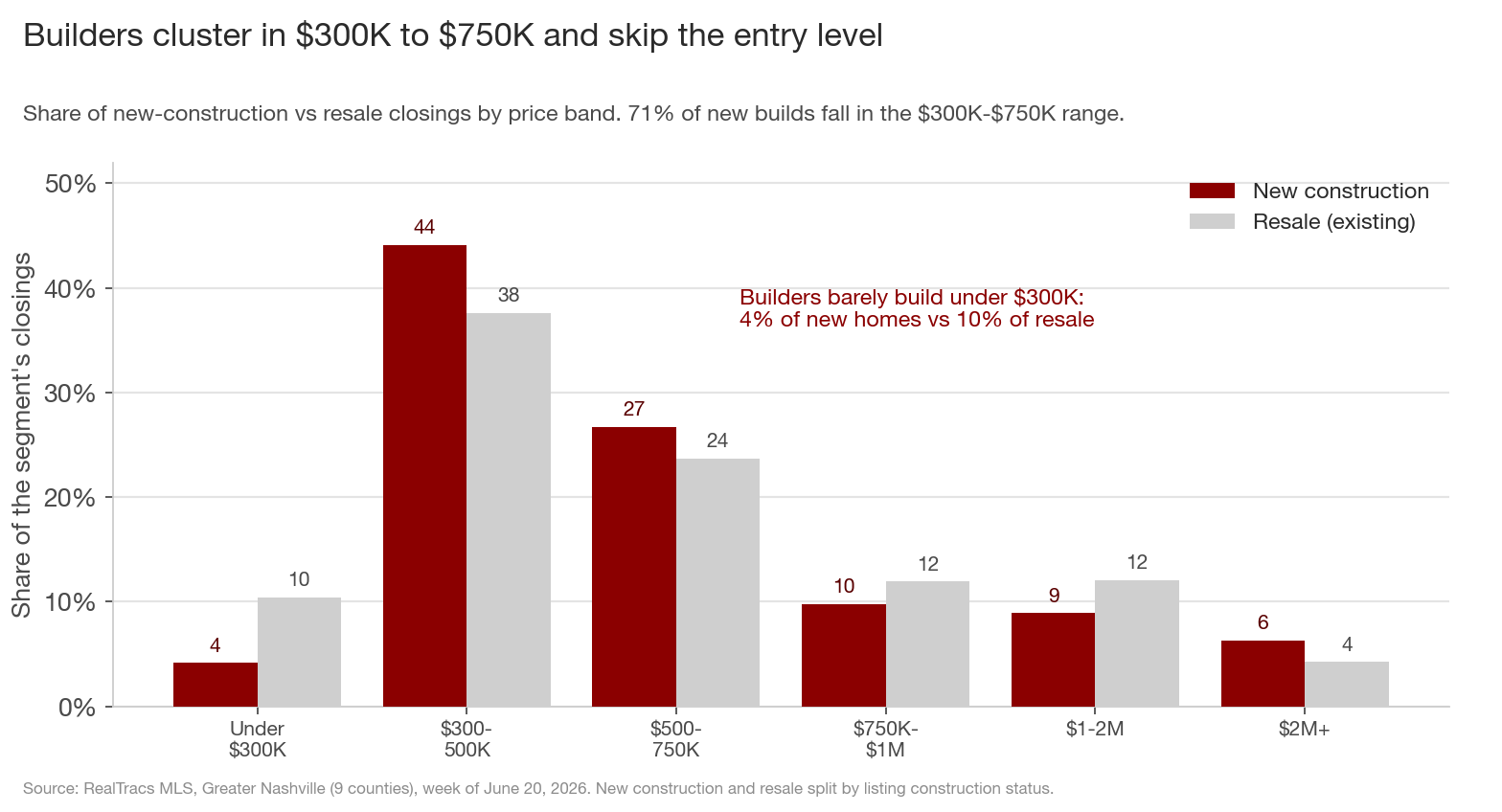

8. Did builders build for the buyer who can least afford 7% rates?

The third force is the clearest in the data, and it ties the others together. Builders did not spread their bets across the market. 71% of new-construction closings fall in the $300K to $750K range, and they have nearly walked away from the true entry level: only 4% of new homes close under $300K, versus 10% of resale, and that sub-$300K share has halved since 2023 (8.3% to 4.2%). The entry-level new home did not vanish so much as climb the ladder into the $300K to $500K band, which by itself is 44% of everything builders sell.

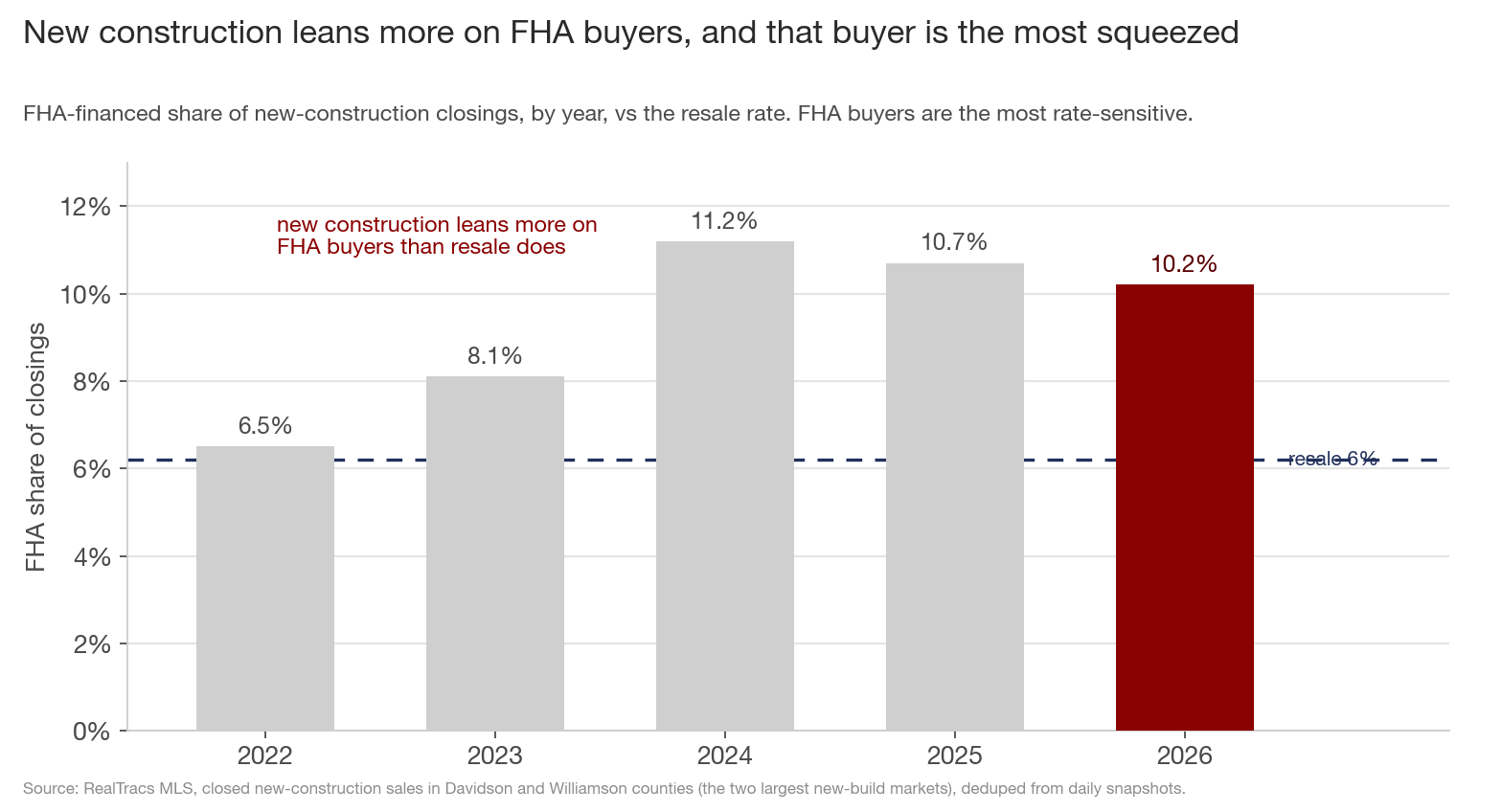

That band runs on the most rate-sensitive buyer in the market. The FHA-financed share of new-construction closings, a stand-in for first-time and lower-down-payment buyers, climbed from 6.5% in 2022 to about 10%, and it sits well above the 6% resale rate. New construction depends on the first-time, payment-stretched buyer more than resale does, and that is exactly the buyer who got knocked out first when mortgage rates parked near 7%. It is the same cohort behind the metro's move-up and middle-band weakness all spring. Builders are over-indexed to the buyer with the least cushion, so when that buyer pauses, new construction feels it before resale does.

It also explains the price discipline from section 3. Cutting the sticker price barely helps a buyer who cannot qualify on the monthly payment, so builders spend instead on rate buydowns and closing-cost credits that lower the payment and keep the FHA buyer in the deal. They are defending their price and their core customer at the same time. (Price-band shares are nine-county; FHA shares are Davidson and Williamson.)

What this adds up to

- One of the market's two halves is still contracting. Resale closings are 10% above their 2023 level (+14% vs 2024); new-construction closings are at a four-year low (-17% vs 2023, -16% vs 2024). New construction's share of all sales has fallen from 26% to 20.9%.

- It's a price-over-volume choice, and demand hasn't collapsed. The median new-build price hit a four-year high of $505K while closings fell 17%; only 21% of new listings have cut price versus 43% on resale, and new-build PPSF is holding (+0.4%) while resale's slips (-1.2%).

- The slowdown has a geography. Builders are still adding inventory in Rutherford (+17%, closings +23%) and Maury (+13%); they're pulling back in Davidson (inventory -7%, closings -20%) and the rural fringe.

- The pipeline points to a lasting shift. New-construction contracts reset about 19% below 2023 and haven't recovered; resale contracts are up 4%. This looks like a lower plateau that has held for two years.

- The base distortion is the wrong explanation here. New-construction closings are down even against the tariff-depressed 2025 comp, and down a sixth against a normal 2024. The weakness is real across every baseline.

- The likely reasons point at one buyer. Three forces plausibly drive the pullback: a product drifting to smaller lots (0.26 to 0.20 acres), national builder reputation under documented strain, and a buyer mix concentrated in the $300K-$750K, FHA-reliant cohort that 7% rates hit hardest. The first two thin the new-build premium; the third explains why new construction softened before resale did.

For buyers, the leverage is lopsided. On the resale side, 43% of sellers are negotiating, which is where the cash-price deals are. On the new-construction side, builders are defending sticker price, so the give is more likely to come as rate buydowns, closing-cost credits, and finish upgrades than a lower number; ask for the incentive rather than the discount, and ask hardest in Rutherford and Maury, where builders are still putting up spec and competing for the same buyers. For builders and developers, the read-through is that the metro has set a clearing rate near 720 new contracts a month at current prices, and the ones holding price are accepting that volume rather than chasing it down; Davidson is the county to watch for the first cuts. For sellers of existing homes, the counterintuitive good news: resale demand is the strongest part of the market right now, but you're competing with a lot of inventory, and the 43% cut rate shows what it's taking to close.

The falsifiable part, to check next month: with new-construction contracts stuck about 19% below 2023, closings should stay near this four-year-low band through summer rather than rebounding, and new construction's share of closings should keep drifting toward 1-in-5 or below. If builders' contracts break back above their roughly 790 ceiling, or their price cuts climb toward the resale 40s (watch Davidson first), that's the signal the price-over-volume strategy is bending. Until then, the resale market is doing the metro's heavy lifting, and Nashville's builders are quietly selling fewer homes for more money, everywhere except Murfreesboro.

Data through the week ending June 20, 2026, Greater Nashville (9 counties: Davidson, Williamson, Rutherford, Wilson, Sumner, Maury, Dickson, Cheatham, Robertson). "Closings" and "contracts" are trailing-31-day counts; "new construction" and "resale (existing)" split listings by construction status, and each year is compared at the same calendar week (late June). Median price is the median closed sale price for newly built homes. Source: RealTracs MLS.